Since 2016, there have been just under 400 founder-led Venture Capital (“VC”) funds created on AngelList alone. Many, if not the majority, are “Dual Threat” founders who are simultaneously running companies and funds. According to AngelList, the top quartile of Dual Threat founders not only vastly outperform the average fund manager on the platform, they are at parity with the top quartile of traditional venture capital firms.

In 2019, I left one of the oldest venture capital firms, Battery Ventures, to partner with two Dual Threat CEOs to start Flex Capital. Our observation was that the best founders were increasingly picking other founders to join their cap table in lieu of traditional VCs. It was catalyzed by 2 major disruptors in venture capital: First by Andreessen Horowitz in 2009 and later by AngelList in ~2015 when they pivoted their focus away from startups raising money on the platform, to a platform for individual fund managers to raise capital and manage their fund vehicles.

Why Is this Happening?

Since 2009, the overarching narrative of venture capital has been the rise of the former founder or executive turned VC. The main pitch is that operators have recent tactical advice for how to run companies, which should be preferred over the theoretical or secondhand wisdom passed on by career investors. Better yet, former founders turned VCs not only offered that wisdom, but also combined it with deep empathy for the founder journey.

This shift has largely been driven by the iconoclastic approach of Marc Andreessen and Ben Horowitz in their formation and growth of A16Z. In particular, the empathy value prop was never clearer than in 2011, when I was a founder and read Ben Horowitz' blog post titled, Nobody Cares.

Andreessen Horowitz brought a seismic shift in venture capital, spurring most incumbent venture capital firms to scale up their fund size, create portfolio services and shift their investing talent to investors with more operating experience. Given the prevalence of this shift, you might expect to find every founder completely satisfied with their VC firm’s offering.

However, that seems far from the current state of affairs.

The venture capital product has never been better. As an entrepreneur, you receive more capital, more portfolio services, and a more empathetic VC partner, for less dilution and less structure. And yet, not too dissimilar to the insatiable appetite of the average American consumer, the goal post for a high NPS score continues to move. Change is the only constant in the technology industry and its adjacent partner, the venture capital industry, is not immune to this dynamic.

Marc Andreessen famously announced that he was “joining the dark side” on Charlie Rose in 2009 and the firm officially “arrived” when The New Yorker profiled Marc in 2015. At roughly the same time as the publication of The New Yorker profile, another seismic shift was occurring in venture capital, which was AngelList.

Where A16Z disrupted the venture capital industry via economies of scale, portfolio services, and marketing, AngelList began quietly disrupting in a method that’s more commonly used by the portfolio companies VCs invest in: software. Through bits (and some legal and tax processes in the background) AngelList obfuscated the complexities around starting a venture capital fund (entity setup, fund admin, tax, etc.). In the process, AngelList democratized access to the venture asset class to a new set of fund managers and limited partners. This shift lacked the PR hoopla that Marc brought to bear but it may end up being just as impactful.

Today, the next logical evolution of venture capital has arrived: founders, ideally CEOs, who are also simultaneously running venture capital funds. They are “Dual-Threat CEOs” who invest and operate companies at the same time. The key driver for this trend is that the bifurcation of time makes them better at both jobs. The operator role exposes them to investment opportunities as they look to leverage cutting-edge technology from startups, connect with other talented CEOs, or even have former employees leave to start their own companies. The investor role exposes them to emerging market trends, operating techniques, and best-in-class operating benchmarks.

The Growth and Success of Dual Threat CEOs

It used to be that founders waited for an exit, then built up an angel track record, and finally rose to be a General Partner at a VC fund. That path has now been compressed so that founders can build their company and simultaneously leverage their natural advantages of being a founder to access and assess startup investment opportunities.

Since the inception of the Dual Threat CEO, there has been substantial growth in the category. According to AngelList, there have been just under 400 Dual Threat funds created since 2016. Through our own research, we've identified nearly 100 former and current Dual Threat funds.

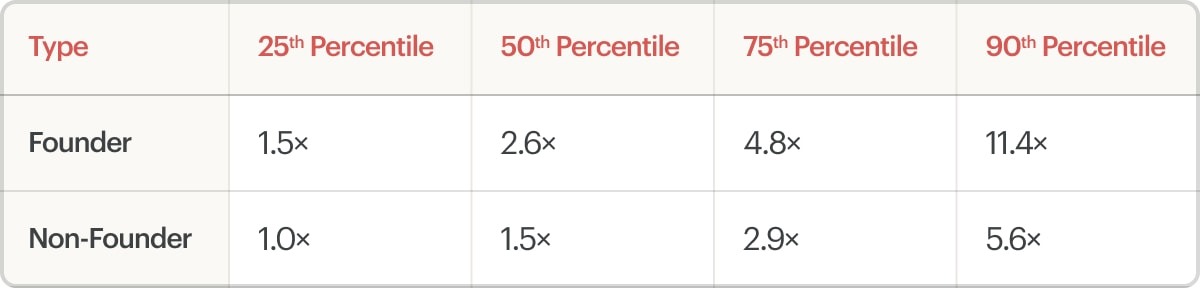

The performance of Dual Threat CEOs is even more intriguing when compared to that of typical venture investors. Proprietary data from AngelList reveals that both the upper quartile and decile, Dual Threat CEOs significantly outperform their counterparts in terms of Multiple of Invested Capital (MOIC). The upper quartile Dual Threat CEOs are as prolific as the best venture firms, who typically fall in the 2.5-3x TVPI range as well. The performance advantage may come from a deeper understanding of technology markets, coupled with the desire from top-tier companies to have a Dual Threat CEO as an advisor.

AngelList Venture Funds w/ Effective Duration 1+ Years

The data is pulled by segmenting Venture Funds that have an effective duration >= 1.0 and cohorting based on the Founder / Non-Founder GP distinction.

Why Is It Differentiated?

I’ve come across many potential explanations to explain why, when bundled with capital, Dual Threat CEOs are a differentiated, or even a better venture product. The most obvious ones are better access to opportunities, more organic connectivity with fellow founders, up-to-date market knowledge from being in the daily flow. What’s stuck out to me is that I’ve never had to actually explain to other founders why it’s better.

Since Flex's inception in 2019, I've shared the Flex "pitch" over 1,000 times and have been struck by how founders instinctively understand the differentiated value of what a sitting CEO and investor would bring, without explanation. Similar to the early days of A16Z, competitive capital sources such as LPs and other venture investors may start as skeptics and are slower to see the differentiated value. Increasingly though, as Dual Threats gain access to more cap tables and put up returns, other GPs and LPs are starting to see Dual Threat CEOs as a complimentary and significant part of the venture capital stack.

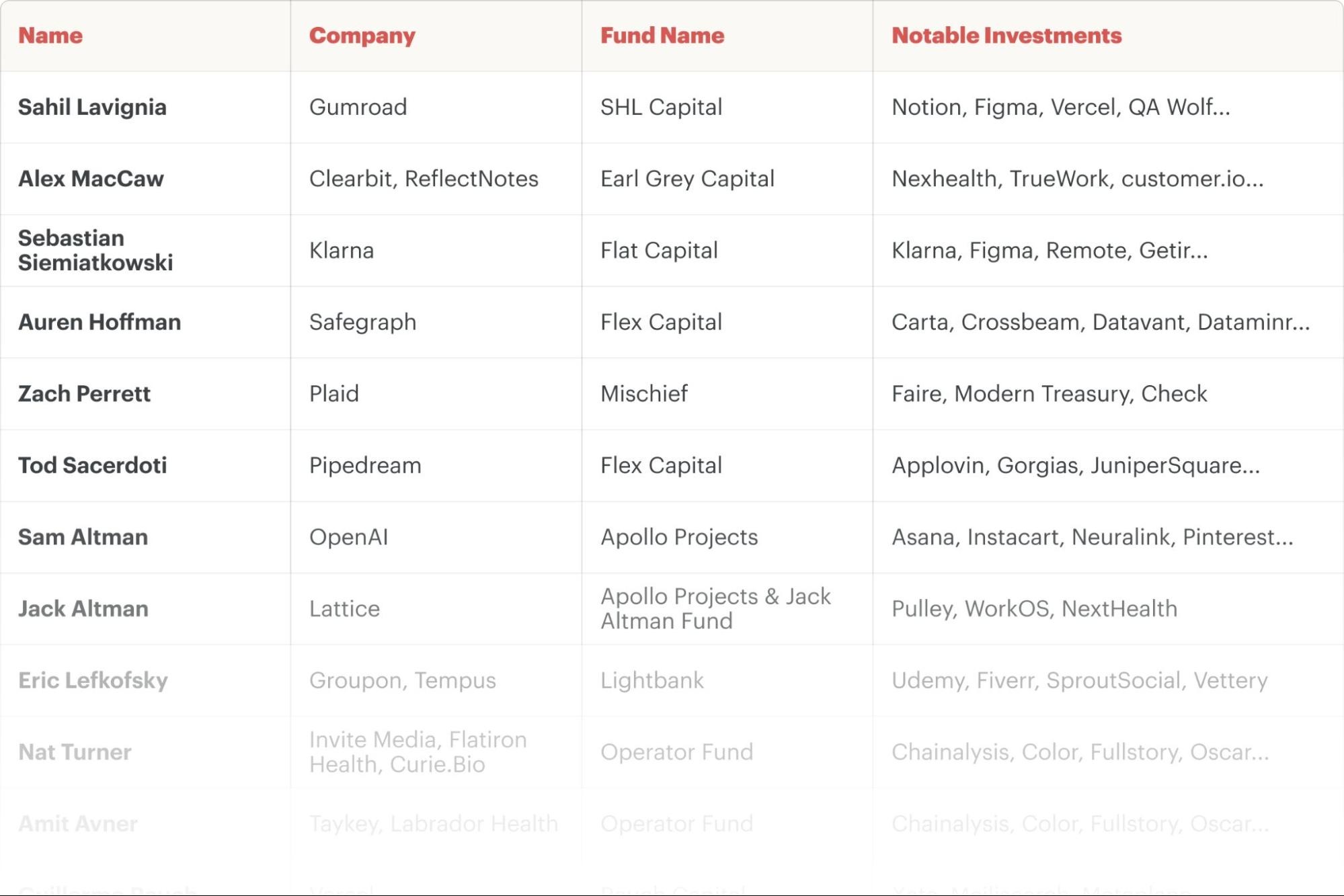

Notable Dual Threat CEOs

(Ordered Alphabetically)

Auren Hoffman and Tod Sacerdoti (Flex Capital) - Both Tod and Auren fit the bill of Dual Threat CEOs. They founded four companies while raising a $200M fund and investing in notable companies like Airbyte, AppLovin, Dataminr, Marqeta, and Masterclass, among others. But as the above chart illustrates, we’re far from the only ones.

Austen Allred (Austen Access Fund) - Austen is the Founder & CEO of BloomTech (fka Lambda School) and the author of the best-selling book, “Secret Sauce”. BloomTech has raised over $120M from investors like Y Combinator, Google Ventures, Bedrock, GGV, Stripe, and Gigafund. Austen began investing through his rolling fund in 2018. Some notable investments include Levels, Maven, Eight Sleep, and Roam Research.

Erik Torenberg (Village Global) - Erik is the founder of On Deck and was previously part of the founding team at Product Hunt. On Deck has raised $70M from investors like Tiger Global and Founders Fund, as well as 200+ Super Angels. Erik began Angel investing in 2014 and formalized his investment efforts in 2017 by starting Village Global, a $500M AUM fund whose portfolio companies have raised more than $5B in follow-on capital.

Guillermo Rauch (Rauch Capital) - Guillermo is the Founder & CEO of Vercel and co-creator of the open source project, Next.js. Vercel has raised $61M from investors like Accel, CRV, Flex Capital, and GV. Guillermo began his angel investing journey in 2016 and has recently established a dedicated fund for his investments. With a keen focus on infrastructure software and developer tools, Guillermo has made seed investments in unicorns like Scale and Auth0.

Immad Akhund (Immad Akhund Rolling Fund) - Immad, a serial entrepreneur, has co-founded four companies and currently serves as the CEO of Mercury. As an active angel investor, he has made notable investments in companies like Rappi, Airtable, and Rippling. Previously, he was a part-time partner at Y Combinator. He now invests out of his rolling fund through AngelList.

Keith Rabois (Founders Fund) - Keith is the CEO and co-founder of OpenStore, which raised $137M from investors like Atomic, Khosla Ventures, and General Catalyst. He is also a General Partner of Founders Fund. Over his career, Keith has held senior executive and co-founding positions at Opendoor, Paypal, LinkedIn and Square. Some of his notable investments include Doordash, Affirm, Ramp and Stripe

Sam Yagan (Corazon Capital) - Sam was the co-founder and CEO of OKCupid which was acquired by Match in 2011. He co-founded Corazon Capital in 2013 while serving as the CEO of The Match Group which he ultimately took public in 2015. After leaving Match in 2016, Sam took over as CEO of ShopRunner led the sale of the business to FedEx in 2020. His notable boards and investments include Duchossois Group, Grindr, Pinterest and Spothero. As a friend and frequent collaborator, we’ve long admired Sam’s entrepreneurial and executive track record.

Conclusion

Dual Threat CEOs are becoming a bigger piece of the Venture Capital ecosystem. They offer a compelling and differentiated product from what incumbent VC firms have built. This unique value prop is clearly resonating, evidenced by the pace of fund formation, investments and track record of Dual Threat CEOs. It’s no longer good enough to be a former CEO because the relevance of prior art around operating VC-backed tech companies deteriorates too quickly. The people who best understand how to operate a company today are currently in the arena, because the game just changes too fast.

.png)

.png)

.png)