“The very name says it all: 'compensation.' If compensation isn't an expense, what is it? And, if real and recurring expenses don’t belong in the calculation of earnings, where in the world do they belong?” - Warren Buffett

The treatment of Stock-Based Compensation (“SBC”) is an old and ongoing debate. That debate seems to have intensified with the tech industry’s propensity to compensate employees with generous SBC packages with the theoretically sound goal of creating more alignment with shareholders.

There have long been rumblings from investors that SBC should be treated more as an operating expense and should be factored into valuation. Meanwhile, management has increasingly argued that SBC is a cash efficient way for money-losing, but fast growing companies to retain talent and is a good tradeoff given how fast share prices have increased.

Despite investors’ stated preference of wanting management to reign in SBC, based on our research, SBC is not factored into valuations.

That could be a mistake.

Do Investors Actually Care?

The Rule of 40 has emerged as a crucial measure of SaaS company performance. This rule adds a company's revenue growth rate to its free cash flow percentage, proposing that their sum should amount to 40% or more for a well-performing SaaS company.

However, the Rule of 40 has faced criticism for its omission of SBC. Since SBC is a non-cash expense, it's typically not factored into the calculation of free cash flow. Our hypothesis is that if investors actually cared about SBC, then a version of the Rule of 40 that included SBC expensed would have a higher correlation to valuation.

A comparative analysis of the Rule of 40, adjusted and unadjusted for SBC, with respect to valuation multiples, shows little difference. In fact, the classic version of Rule of 40 has a higher correlation to valuation multiples than its SBC inclusive counterpart. This implies that not only do the public markets not penalize tech companies for high SBC costs, but they even tend to value them based on adjusted profitability metrics.

Further, analysis of SBC as a percentage of sales (SBC/LTM %) in relation to valuation multiples suggests no substantial correlation between these two variables. This further substantiates the argument that the public markets do not consider SBC as a significant factor when valuing companies.

Why Investors Should Care

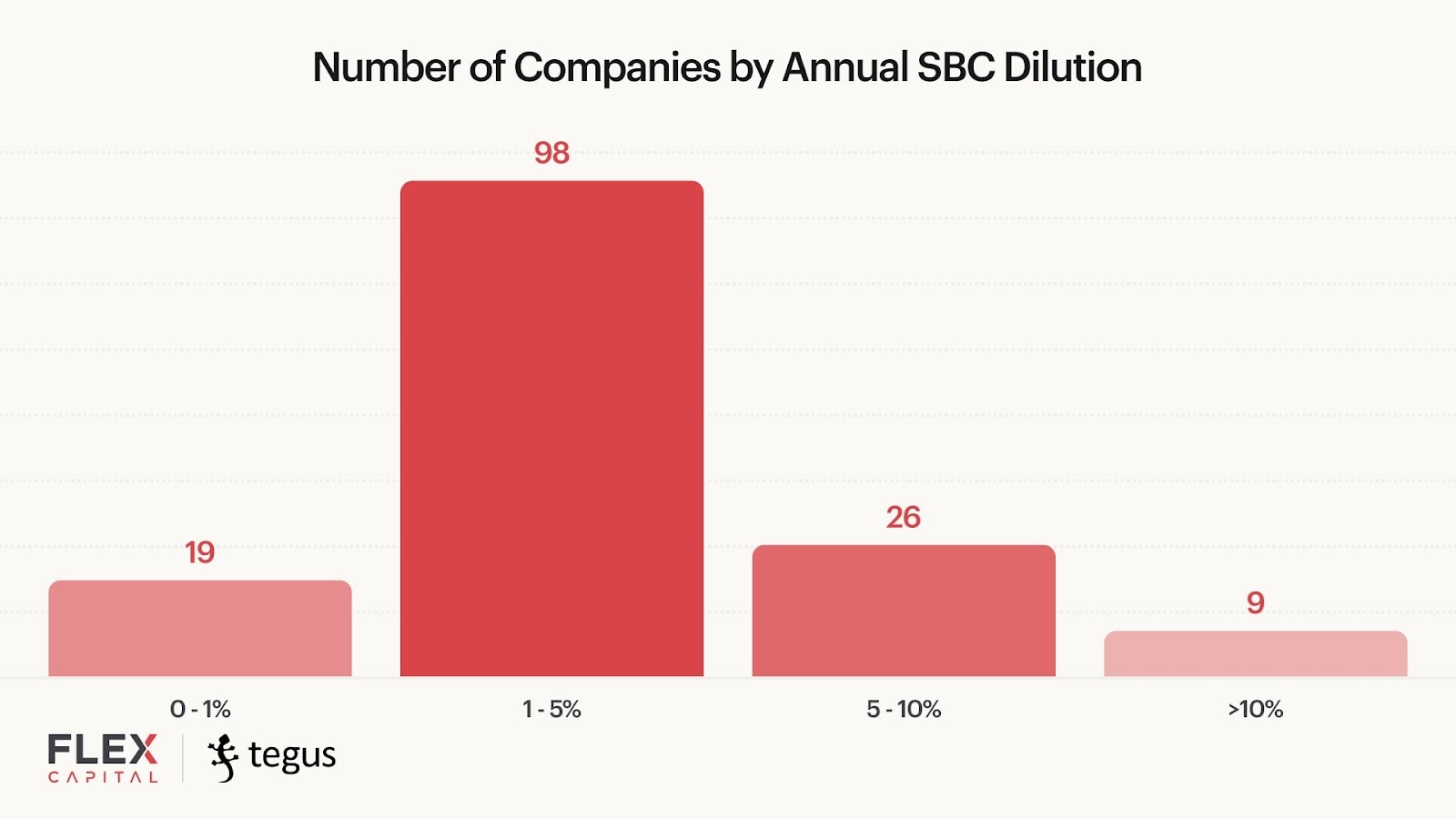

There is an important consideration that isn’t captured in the graphs above. For each dollar of SBC, there is dilution for the existing shareholders. As a result, investing in two companies with the exact same enterprise value growth can have drastically different returns due to SBC. In the end, many companies conduct share buy backs to fight dilution, but this can end up becoming a major cash cost too. For public SaaS companies, most are diluting between 1-5% yearly with a handful of companies stretching over 10%.

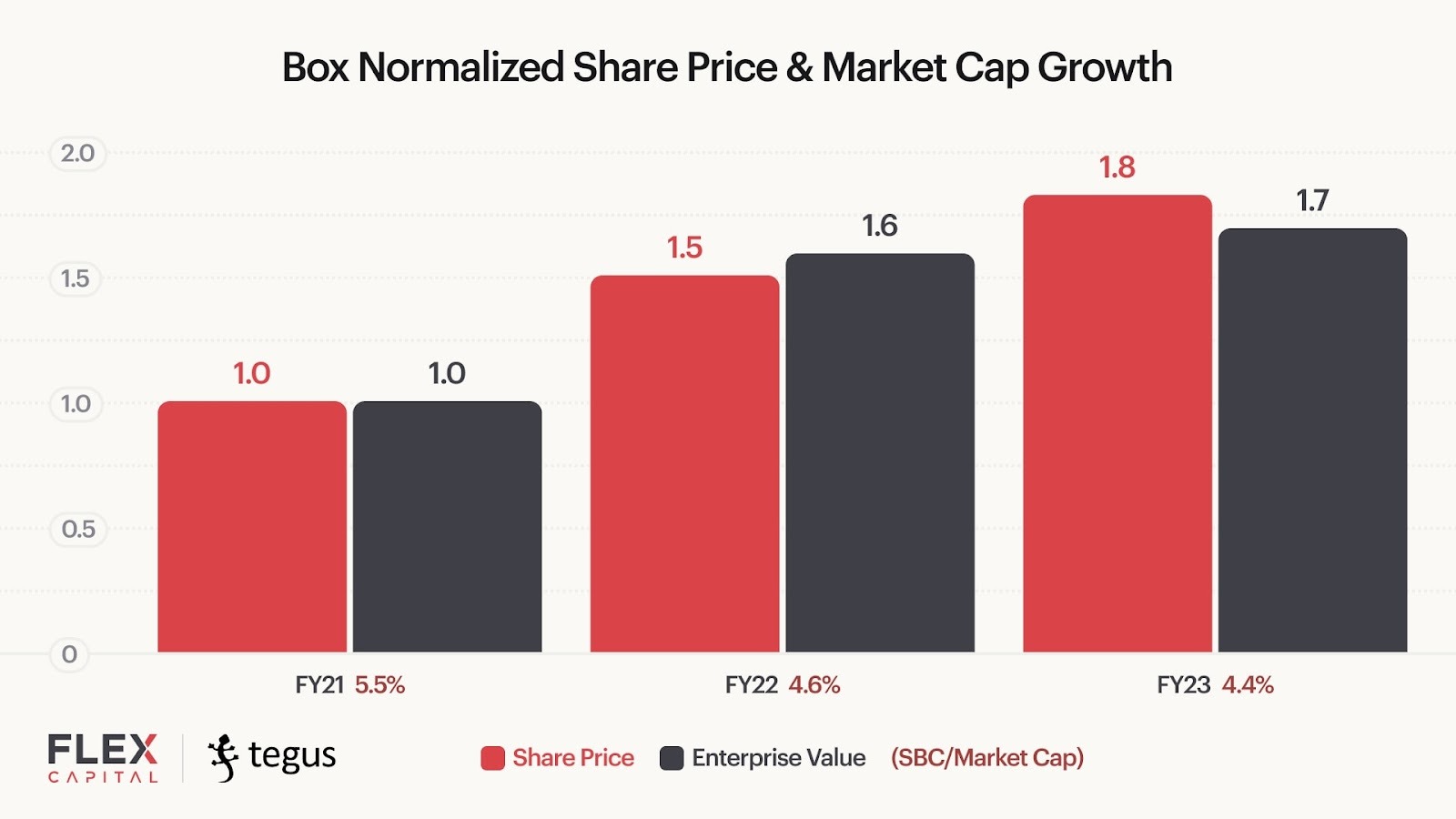

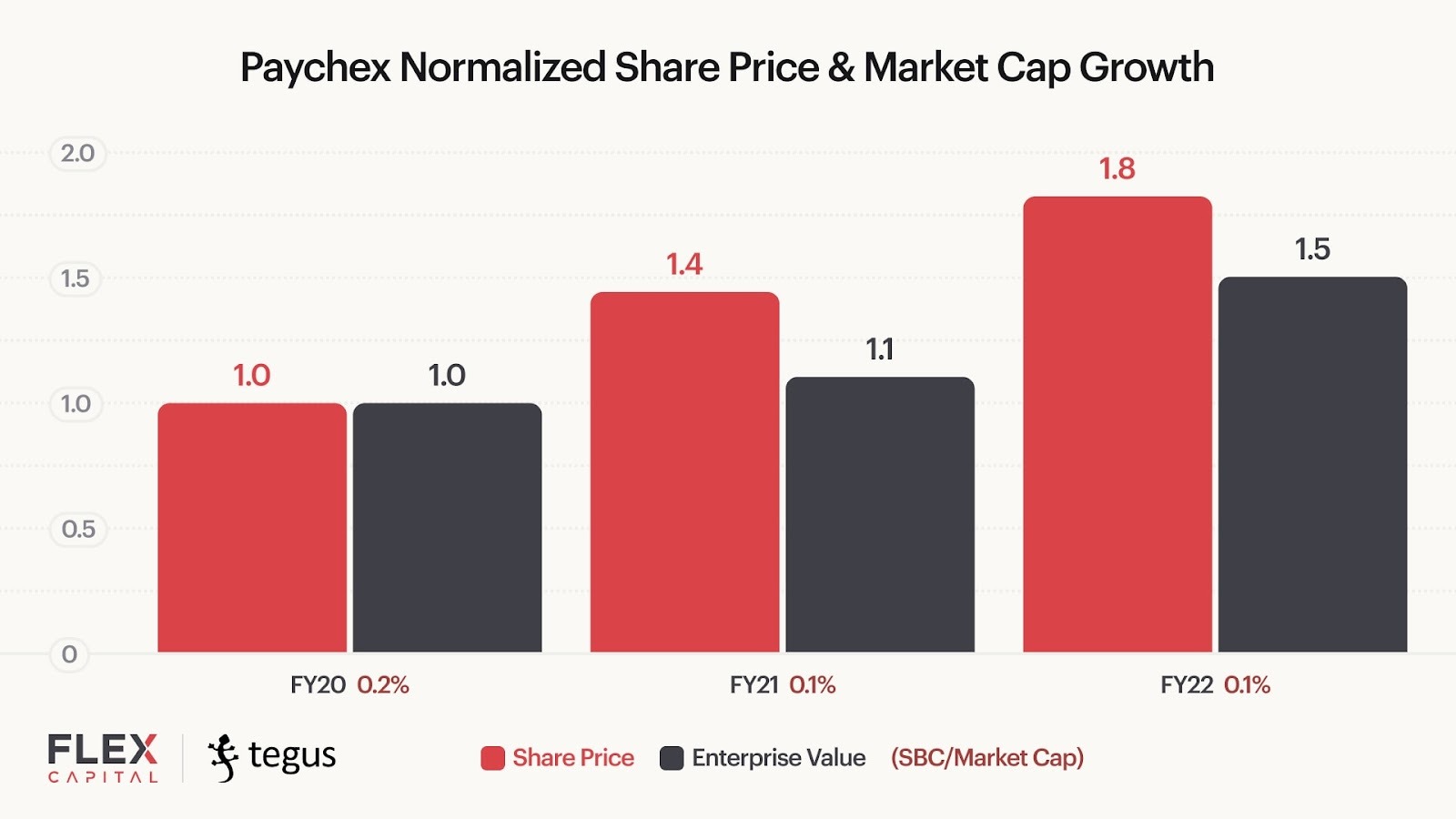

Consider the example below, where you can see the share price trajectory of Box and Paychex over a 3 year period. Despite Box achieving almost 50% higher enterprise value growth than Paychex, both companies had the same share price increase. Clicking one level deeper, you can observe that much of this stems from a substantially higher SBC dilution from Box.

The Expense Argument

The Box vs. Paychex example supports the school of thought which argues that SBC should be treated no differently than cash bonuses and other forms of remuneration, classifying it as an operating expense. This perspective stems from the logic that SBC represents a cost to the company in the form of equity given to employees.

In light of the tech boom, regulators adopted a similar stance. Historically, companies weren't required to recognize SBC as an expense on their income statements. However, this changed in 2004 when the Financial Accounting Standards Board (FASB) issued the Statement No. 123R, mandating companies to calculate the fair value of the equity instruments they give to employees, recognizing that as a compensation expense in their financial statements.

The Capital Allocation Argument

The counter-argument views SBC as a capital allocation exercise akin to issuing new shares for raising capital. This interpretation proposes that SBC doesn't impact a company's cash flows directly and should, therefore, be considered separately from typical operating expenses.

Reflecting this perspective, most technology companies report adjusted profitability metrics alongside the GAAP-mandated measures, often excluding SBC from their calculations of operational cash flow or profitability.

Our Position

SBC is a powerful and necessary tool for private and public companies to recruit and align incentives with employees. Like cash, it is a form of compensation, but it often gets overlooked.

If management and investors are not diligent about cash compensation, the company may end up destroying shareholder value, or worse go bankrupt. Similarly, if they are not diligent about SBC compensation, they could find their ownership completely diluted.

There should be a healthy balance around SBC treatment, and empirically, the current public investing behavior suggests that investors may be too lenient. Despite being a prominent feature of tech company compensation structures, it does not appear to be a strong factor in public market investors’ valuation of such companies.

Special thanks to Canalyst at Tegus for having a seamless platform to access all of the data found in this article. We were pleasantly surprised to learn that besides expert call transcripts, Tegus has an expansive data set for public market companies which can be accessed via an excel plugin. - you can trial the platform here.

.png)

.png)

.png)